What Is a Wind Mitigation Inspection? Why They Matter in FL

A wind mitigation inspection is a formal evaluation of how well your home is built to resist hurricane-force winds. A licensed inspector reviews key structural features (your roof shape, deck attachment, wall connections, and opening protection), then documents the findings on a standard state form that your insurance company uses to calculate discounts.

For Florida homeowners, this is one of the most practical inspections you can get. Florida law requires insurers to offer discounts for qualifying wind-resistant features, but you have to prove those features exist before any discount applies.

At Inside & Out Property Inspectors, we perform certified wind mitigation inspections across Northeast Florida, including Jacksonville, St. Augustine, and the surrounding communities. This post covers what inspectors look at, how the report affects your premium, and what to expect on inspection day.

What Does a Wind Mitigation Inspection Focus On?

A wind mitigation inspection is not a general home inspection. It does not evaluate your HVAC, plumbing, or electrical systems. Instead, it focuses entirely on how well your home can hold up during a high-wind event like a hurricane or a severe tropical storm.

The goal is simple: document the wind-resistant features your home already has. Those features get submitted to your insurance company as proof. If they meet the criteria, you qualify for credits that reduce your premium.

The inspection is documented on Florida’s Uniform Mitigation Verification Inspection Form, known as the OIR-B1-1802. This form was created by the Florida Office of Insurance Regulation and is the standard used by every insurance company writing policies in the state. Every Florida home inspector certified to perform wind mitigation inspections uses this same form.

What Does the Inspector Check?

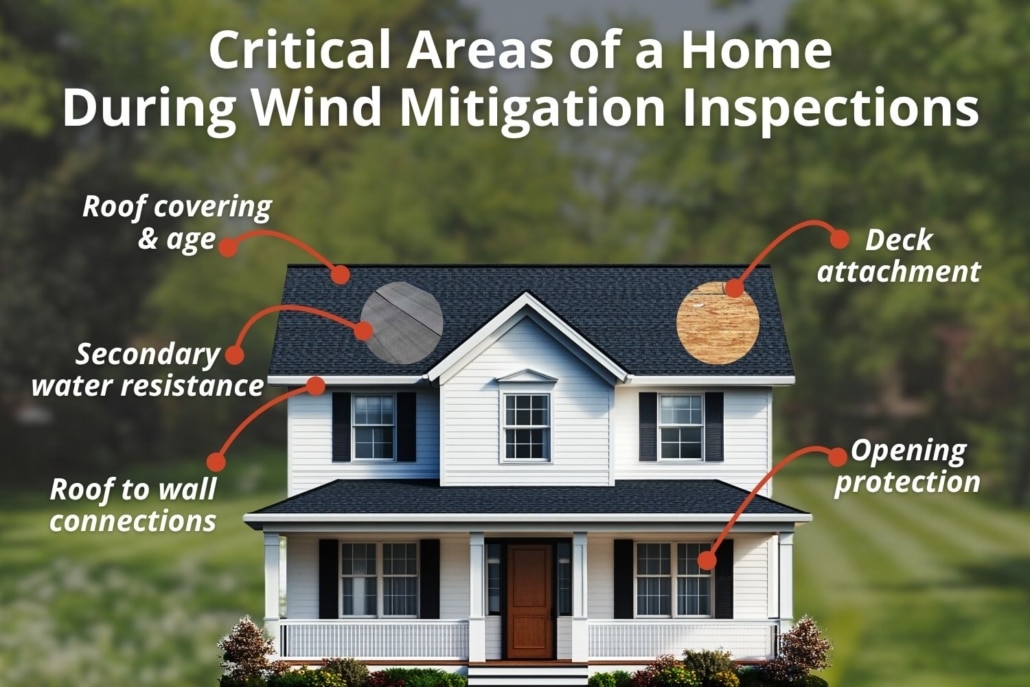

The OIR-B1-1802 covers seven areas of your home. Each one represents a potential insurance discount:

- Building code and year built: Homes built after March 1, 2002, were constructed under the Florida Building Code, which sets higher wind-resistance standards. This alone often qualifies you for a discount.

- Roof covering: The type of roofing material and when it was installed. A newer roof, especially one installed after 2002, typically earns better credits.

- Roof deck attachment: How the plywood or OSB roof deck is fastened to the framing. Larger nails with tighter spacing mean a stronger attachment and a better score.

- Roof-to-wall attachment: The connectors holding your roof structure to your walls. Clips, single wraps, and double wraps each carry different weights. Double wraps are the strongest and earn the highest discount.

- Roof shape: Hip roofs, where all four sides slope downward to the walls, perform significantly better than gable roofs in high winds. Testing has shown hip roofs can receive up to 40% less wind pressure than gable roofs.

- Secondary water resistance (SWR): A sealed underlayment or foam barrier on the underside of your roof deck. This is a backup layer that prevents water from getting in if shingles blow off during a storm.

- Opening protection: How your windows, doors, garage doors, and skylights are protected. Impact-resistant glass and hurricane shutters both count here.

The inspector will need access to your attic to check items three and four. Make sure attic access is clear before your appointment!

The OIR-B1-1802 Form Explained

The 1802 form has been through several versions. As of April 2026, the Florida Office of Insurance Regulation released an updated version of the form, which is now the required standard. If you have an old report sitting in a drawer, check when it was completed. Reports are valid for five years, but your insurer may request an updated inspection if the form version has changed.

Photos are required for every feature documented on the form. An inspector who does not take photos or who skips the attic cannot properly complete the form. Be cautious of very low-cost inspections that cut corners here: insurers can and do reject incomplete forms.

How a Wind Mitigation Inspection Affects Your Insurance

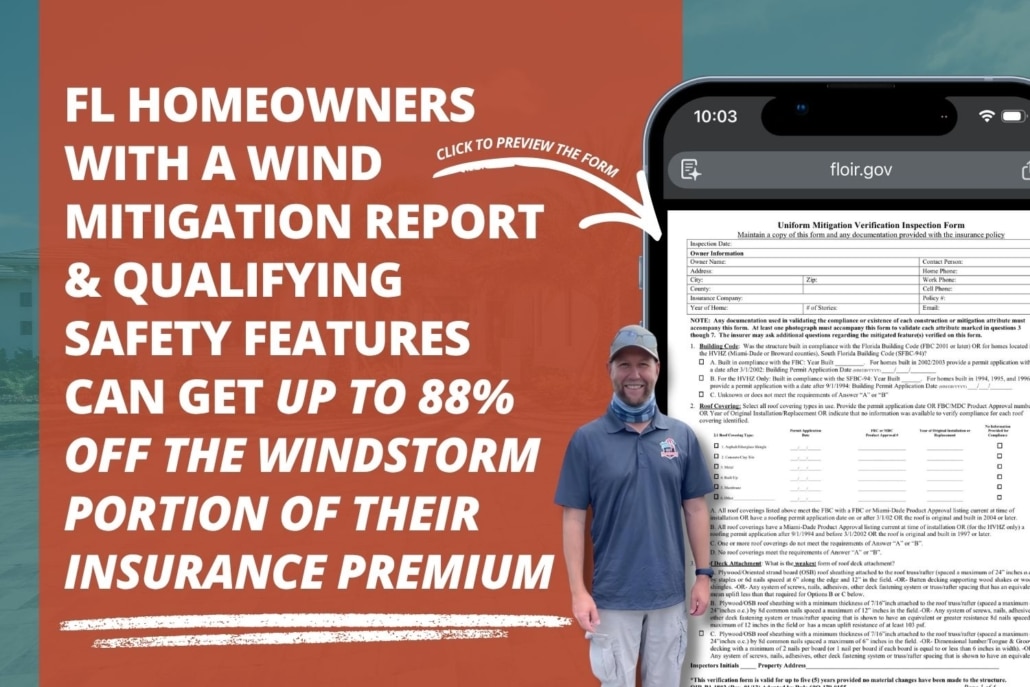

Florida law requires all residential property insurers to offer premium discounts for qualifying wind-mitigation features. The discounts are not automatic. You have to submit a completed wind mitigation report to trigger them.

The savings vary by insurer and by the features your home has, but they can be meaningful. A strong report, with a hip roof, impact windows, double-wrap roof straps, and a secondary water barrier, can reduce your wind insurance premium by 30–45%. In Florida, wind coverage can make up 80% of your total homeowner’s insurance premium, so even a 20% discount translates to real money.

If you have never filed a wind mitigation report, you are likely paying the full undiscounted rate.

What Discounts Are Possible?

Each of the seven sections on the OIR-B1-1802 form is a potential discount. Your insurer calculates a credit based on the combination of features documented. The highest credits typically go to homes that have all of the following:

- A hip roof

- Roof deck attached with 8d nails at 6-inch spacing or tighter

- Double-wrap roof-to-wall connectors

- A secondary water resistance barrier

- Impact-rated windows, doors, and garage doors on all openings

Not every home will qualify for every credit. Older homes with gable roofs and single-pane windows may still qualify for partial credits based on roof age and construction quality.

Homes Built After 2002 vs. Older Homes

If your home was built after March 1, 2002, it was constructed under the Florida Building Code and is far more likely to qualify for multiple discounts. Newer construction tends to have tighter roof deck attachment, modern straps, and often impact-rated openings as standard.

Older homes are still worth inspecting. A home built between 1974 and 2002 may have some qualifying features, especially if the roof has been replaced since 2002. If your roof was replaced with modern materials and proper attachment, a wind mitigation inspection can document that and unlock credits you would otherwise miss.

What to Expect During the Inspection

A wind mitigation inspection typically takes 30 to 60 minutes for an average-sized Florida home. Here is what happens:

- The inspector arrives and confirms your address and any permits or documentation you have on hand (roof permits, product specs, or notice-of-acceptance letters for impact windows can help).

- They walk the exterior to assess roof geometry, roof covering, and any visible opening protection.

- They access your attic to inspect the roof deck attachment and roof-to-wall connections, and take required photos.

- They document any shutters, impact doors, or other opening protection on all sides of the home.

- You receive the completed OIR-B1-1802 form, with photos attached. Most inspectors deliver the same day or within 24 hours.

You do not need to be on the roof or in the attic yourself. The inspector handles all of that. Your main job is to make sure attic access is clear and that you have any relevant documentation ready.

Many Jacksonville and St. Augustine homeowners bundle a wind mitigation inspection with a 4-point inspection at the same time. Both are common requirements for Florida insurance renewals, and combining them saves a second appointment.

How Long Is a Wind Mitigation Report Good For?

A completed wind mitigation inspection report is valid for five years from the inspection date, as long as no material changes have been made to the structure.

If you replace your roof, install impact windows, or make any other structural upgrades during that window, you should get a new inspection. Those improvements will likely improve your score and earn you better discounts.

If you switch insurance companies during the five-year window, your new insurer may request a fresh inspection. Not all carriers accept older reports at policy transfer, so ask before you assume the old report transfers.

Set a reminder five years out. A lapsed wind mitigation report means you lose your discounts at renewal and will need to schedule a new inspection to get them back.

Related Questions to Explore

Is a wind mitigation inspection required in Florida? No, it is not required by law. However, Florida law does require insurers to offer discounts for homes with qualifying wind-resistant features. The only way to claim those discounts is to submit a completed wind mitigation report. So while the inspection is optional, skipping it likely means paying a higher premium than you need to. For most Florida homeowners, the inspection cost pays for itself in the first year.

What does a wind mitigation inspector look for? The inspector evaluates seven specific areas of your home: when it was built, your roof covering and its installation date, roof deck attachment method, roof-to-wall connection type, overall roof shape, whether a secondary water resistance barrier is present, and what protection exists on your windows, doors, garage doors, and skylights. Each area can qualify for a separate insurance discount. Learn more about what is covered on our wind mitigation inspection service page.

What is the difference between a wind mitigation and a 4-point inspection? A wind mitigation inspection focuses only on your home’s ability to resist wind damage and is used to unlock insurance discounts. A 4-point inspection looks at four major systems (roofing, electrical, plumbing, and HVAC) and is typically required by insurers before they issue a new policy on an older home. The two inspections have different goals and use different forms. Many Florida homeowners need both, and scheduling them together is the most efficient option.

When to Call a Professional

A wind mitigation inspection is not a DIY project. Florida law specifies exactly who can complete the OIR-B1-1802 form: licensed home inspectors with hurricane mitigation training, building code inspectors, licensed general or building contractors, professional engineers, and licensed architects. The inspection must also be performed by the individual holding the license, not a staff member working under them.

Beyond the legal requirement, the quality of the inspection matters. An inspector who skips the attic cannot document your roof deck or roof-to-wall connections, which means you lose two of the largest discount categories on the form. Photos are required for every feature. If your inspector does not produce a photo-backed report, your insurer can reject it.

If you are buying a home in Northeast Florida and your agent has not mentioned a wind mitigation inspection, bring it up. It is one of the most cost-effective add-ons to a pre-purchase inspection, and a strong report can be used as a negotiating tool at closing.

BJ Johnson and the team at Inside & Out Property Inspectors are certified to perform wind mitigation inspections in Jacksonville, St. Augustine, Ponte Vedra, Neptune Beach, and across Northeast Florida. We are InterNACHI Certified Master Inspectors with InterNACHI’s wind mitigation certification.

Also good to keep in mind:

If a recent storm has caused roof damage, a standard home inspection can assess the full scope before you file a claim.

Conclusion

A wind mitigation inspection is a small investment with a long payoff window. For most Florida homeowners, the $75–$150 inspection cost comes back in insurance savings within the first year, and the report stays valid for five years.

Key takeaways:

- The inspection documents wind-resistant features your home already has. You do not need to make repairs first.

- It uses Florida’s standard OIR-B1-1802 form. Every insurer in the state accepts it.

- Reports are valid for five years, or until you make structural changes.

If you are in the Jacksonville or St. Augustine area and have never had a wind mitigation inspection, or if your report is approaching the five-year mark, now is a good time to schedule one. Visit our wind mitigation inspection page to learn more.